The CIPD’s Labour Market Outlook is a forward-looking indicator of the UK labour market. It is a quarterly survey of 2,000 employers, providing analysis on employers’ recruitment, redundancy and pay intentions combined with unique insights on labour market topics.

The Labour Market Outlook report is released every February, May, August and November. However, the data from it is also included in other reports, blog posts and thought pieces. Its survey insights feed into our consultations with UK Government.

On this page, you’ll find links to key content and communications that use Labour Market Outlook data.

Labour Market Outlook report

Winter 2023-24 overview

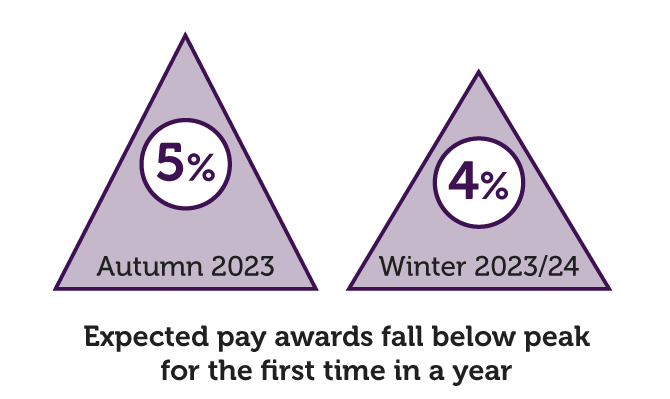

This quarter, we see the tide turning on pay. For over a year, expected basic pay awards for the upcoming 12 months have been at 5%. This quarter, they have fallen to 4%, matching the level of CPI inflation reported in the 12 months to December 2023.

Decreasing staff levels is higher on the agenda in 2024, in response to the higher wage costs experienced over the past couple of years. This is evident in both the public and private sector.

Labour market tightness is meanwhile reducing. Our data show there will be further easing in the coming months, as fewer employers are expecting significant problems filling vacancies going forward.

Read on for our latest labour market data and analysis on employers’ recruitment, redundancy and pay intentions this winter.

Winter 2023-24 video summary

Key findings

|

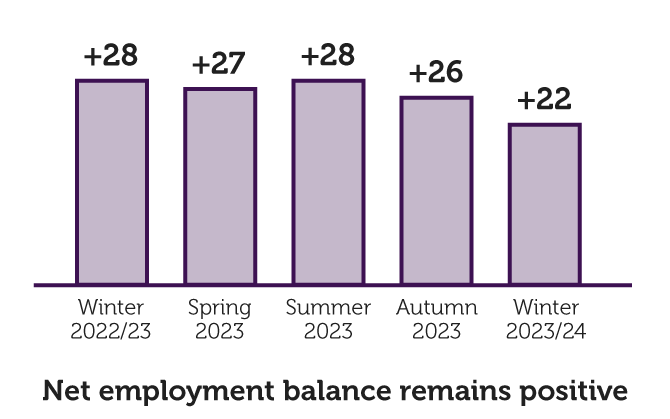

Net employment balance remains positiveThe net employment balance – which measures the difference between employers expecting to increase staff levels in the next three months and those expecting to decrease staff levels – remains positive but has fallen from +26 last quarter to +22 this quarter. |

|

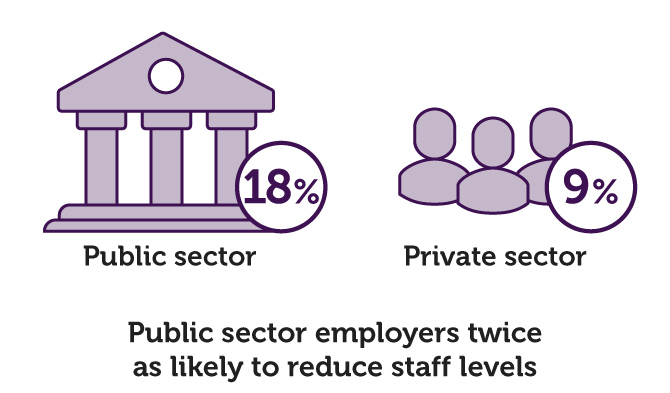

Public sector employers twice as likely to reduce staff levelsNine per cent of private sector employers plan to decrease staff levels in the next three months. The rate is twice as high in the public sector, where 18% of employers plan to decrease staff levels in the next three months. |

|

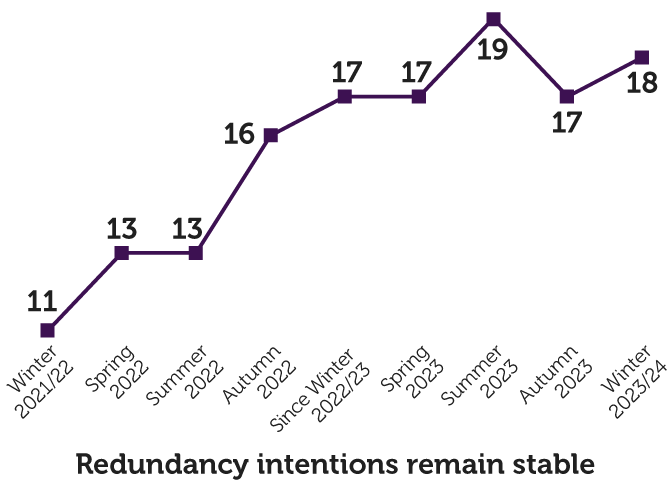

Redundancy intentions remain stableOverall, 18% of employers are planning to make redundancies in the three months to March 2024. |

|

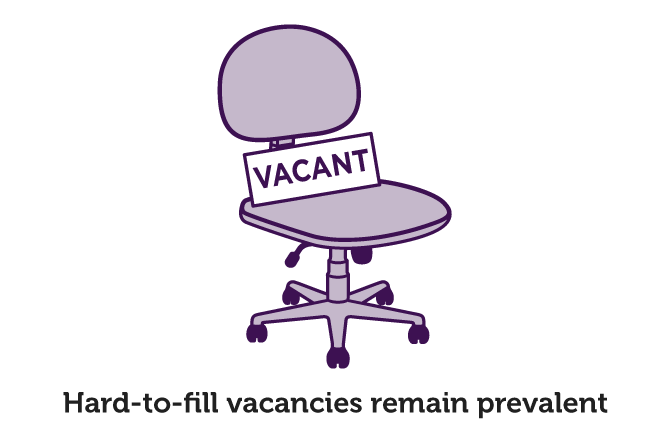

Hard-to-fill vacancies remain prevalentThirty-eight per cent of employers surveyed have hard-to-fill vacancies. Hard-to-fill vacancies are significantly higher in the public sector (51%) than the private sector (34%). |

|

Expected pay awards fall below peak for the first time in a yearThe median expected basic pay increase has fallen from 5% last quarter to 4% this quarter. Expected pay awards in the public sector fell further than in the private sector to 3%. |

Media centre

Are you a journalist looking for expert commentary and insights on the world of work?

Topics A-Z

Browse our A–Z catalogue of information, guidance and resources covering all aspects of people practice.

Related content

Our Labour Market Outlook survey findings play an important role in shaping our content and communications on a wide range of topics and focus areas at the CIPD. Our survey findings achieve this by providing labour market insights that support broader discussions on topics including staff morale, pay transparency, generative AI and financial wellbeing.

CIPD research shows varied responses to generative AI use from organisations, as some explore opportunities to improve productivity

Mark Beatson looks at the latest data on staff morale in the public sector and finds that it’s declining, driven by excessive workloads and staff shortages

Charles Cotton analyses CIPD data on pay transparency to uncover how many employers have decided to be transparent about pay, and what motivates that decision

Charles Cotton addresses the question of what constitutes a reasonable National Living Wage, by analysing the CIPD Labour Market Outlook – Summer 2023 report