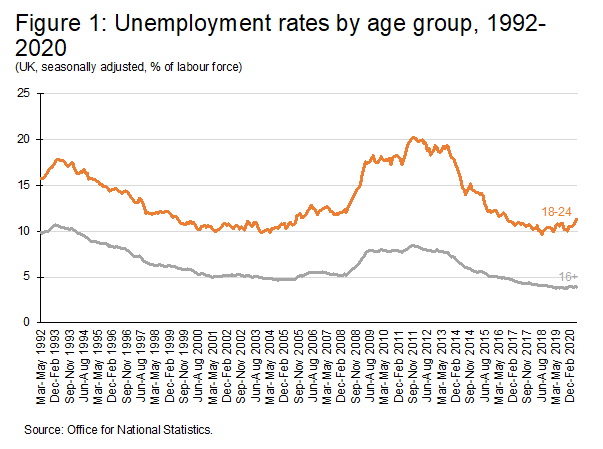

Recessions are typically bad news for young people, especially school and college leavers. After the financial crisis, the unemployment rate of those aged 18–24 increased faster than that of all adults (Figure 1).

Low growth in productivity and wages

In addition, subsequent low growth in productivity and wages meant that progression for people entering the labour market then was less than for previous generations of young people.

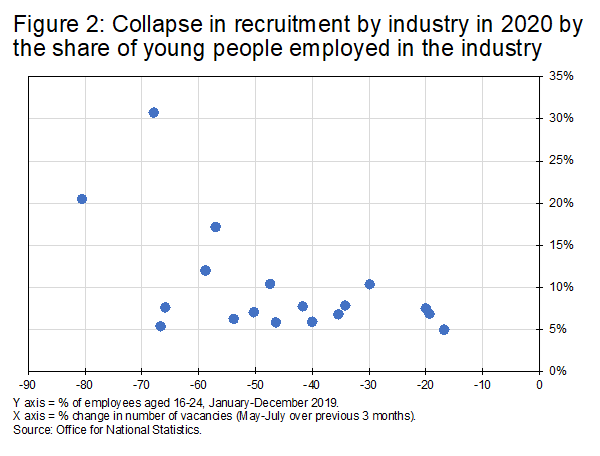

The COVID-19-inspired recession has been no exception. The industries hardest hit by this recession were those which, pre-pandemic, were most likely to employ young people (Figure 2).

The two industries with the highest proportions of employees aged under 25 – Accommodation & Food and Arts, Entertainment & Recreation – were the industries most affected by the pandemic, with vacancies down two-thirds or more. According to the Resolution Foundation, young people were also more likely to be furloughed than older age groups. And, although there could be issues concerning the reporting of data under lockdown, apprenticeship starts appear to be well down on last year.

Steps the Government is taking

Some of the measures taken to protect employment during lockdown could make the situation worse for young people out of work. In particular, the Job Retention Scheme could have discouraged both redundancies and fresh recruitment in those industries affected most by the pandemic.

Hence it is no surprise that the Chancellor’s Plan for Jobs included specific proposals for hiring young people, in addition to measures – such as Eat Out to Help Out – designed to stimulate activity in industries that employ lots of young people.

Two of these proposals – increasing the financial incentives for employers to take young people on apprenticeships and traineeships – essentially turn up the volume on existing mechanisms, though whether these go to eleven is a matter of opinion. Not all the barriers to taking more young people on through these routes will, however, be financial. For example, the workplace-based components of apprenticeships may be challenging to deliver in organisations with much more remote working. Simply paying employers more doesn’t guarantee a solution to all problems.

For these reasons, the Plan proposed a new initiative, the Kickstart scheme, targeted at unemployed 18-24 year olds claiming Universal Credit. Details are still emerging, but the scheme publicity says it will offer work placements of up to six months, with the cost of wages (up to the relevant minimum wage) paid by the Government.

What now?

Take-up will be an issue. Will employers want to offer placements? An online poll of CIPD members found that only a fifth thought it likely or very likely that their organisation could accommodate Kickstart placements, whereas three-fifths thought it unlikely or very unlikely. It’s difficult to know what to make of these numbers. They don’t sound great but employer participation in schemes of this kind has always been a problem, with most placements tending to be in the public and voluntary sectors.

Nor should participation by young people be taken for granted. Previous recessions have seen young people try to “hide” in full-time education until economic conditions improve. If this year’s A Level results furor encourages more young people to stay for a while in education, it may prove to be a blessing in disguise.

Topics A-Z

Browse our A–Z catalogue of information, guidance and resources covering all aspects of people practice.

Bullying

and harassment

Discover our practice guidance and recommendations to tackle bullying and harassment in the workplace.

About the author

Mark Beatson, Senior Labour Market Analyst

Mark's respected labour market analysis and commentary strengthens the CIPD’s ability to lead thinking and influence policy making across the whole spectrum of people management and workplace issues.

Prior to joining the CIPD, Mark was an economic consultant and for over 20 years worked as an economist in the Civil Service, latterly at Chief Economist/Director level, in a range of Government departments including the Department for Business Innovation and Skills (BIS), the Department for Innovation, Universities and Skills (DIUS), the Department of Trade and Industry (DTI) and HM Treasury.

Peter Cheese, the CIPD's chief executive, looks at the challenges and opportunities faced by today’s business leaders and the strategic priorities needed to drive future success

Insight from the CIPD’s survey into factors driving pay decisions in UK workplaces and recommendations for practice

We examine people’s desired hours and how this compares to the hours they actually work

Peter Cheese, the CIPD's chief executive, looks at the challenges and opportunities faced by today’s business leaders and the strategic priorities needed to drive future success

We outline the key pieces of legislation set to come into force in the UK and explain their implications for employers and employees

We examine people’s desired hours and how this compares to the hours they actually work

Employers’ reactions to pension proposal highlight concerns over cost, while the CIPD calls for focus on raising pension awareness among staff, the need for higher contributions and better understanding of value for money