In last week’s Budget the Chancellor revealed that poor levels of productivity, according to forecasts from the Office for Budget Responsibility (OBR), would mean that the UK’s Gross Domestic Product (GDP) would grow by 5.7% over the next five years. This was down from the predicted 7.5% growth expected back in March. He told the House of Commons:

…regrettably our productivity performance continues to disappoint.

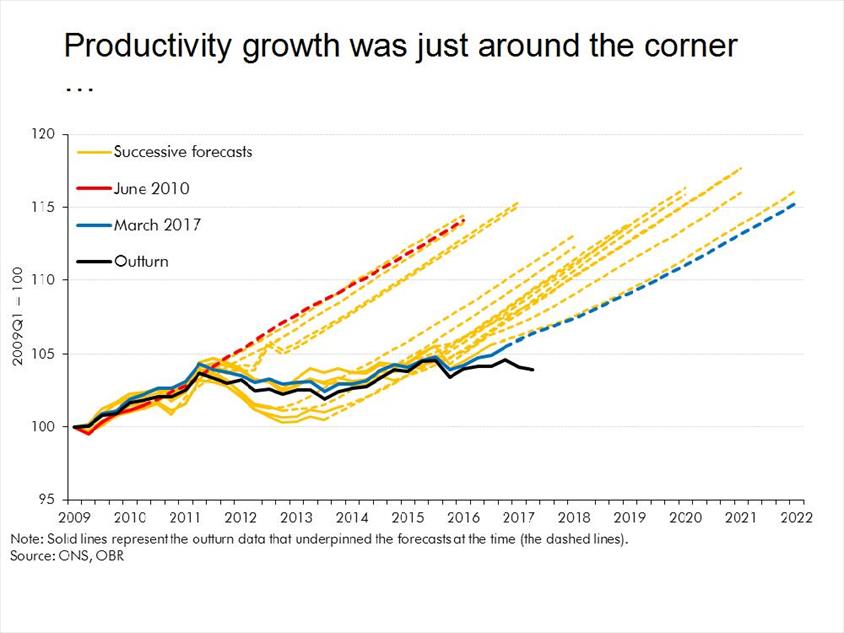

The OBR has assumed at each of the last 16 fiscal events that productivity growth would return to its pre-crisis trend of about 2% a year, but it has remained stubbornly flat.

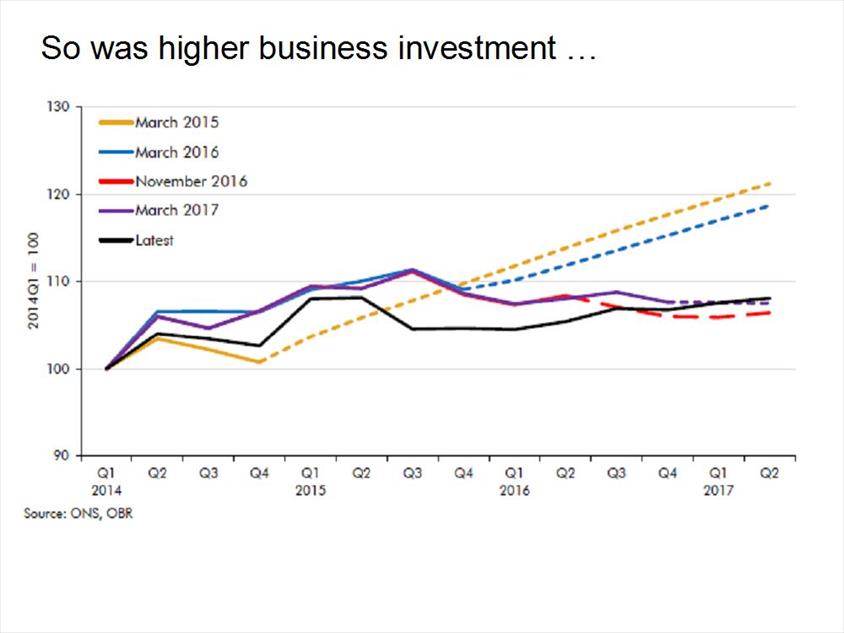

So today they revise down the outlook for productivity growth, business investment, and GDP growth across the forecast period.

The news about productivity yesterday, however, wasn’t entirely unexpected. This was because last month saw the OBR publish its October 2017 Forecast Evaluation Report. It compares its twice-yearly economic and financial forecasts against what happened and tries to find out why forecasts went awry. For such a technical report, it got a lot of media coverage, such as coverage in the Independent and on the BBC.

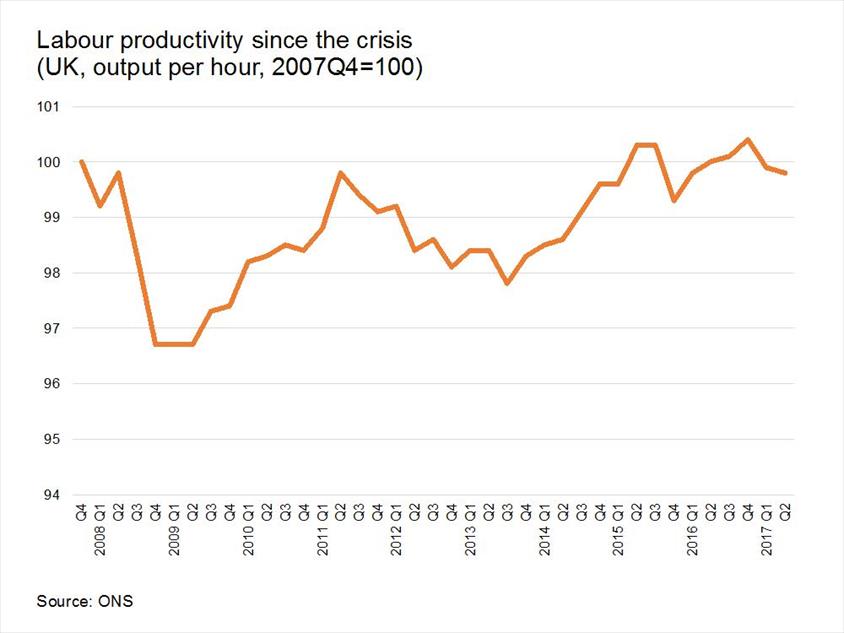

The reason for this level of coverage was that the report looked at our labour productivity growth and recognised it wasn’t just hiding behind the corner – it had gone missing. As the chart below shows, labour productivity – measured by output per hour – peaked just before the financial crisis, in 2007 Q4. It briefly exceeded that level in 2015 and 2016, but fell in the first two quarters of 2017.

The OBR expected productivity to fall during the recession (this usually happens), but they also expected it to bounce back towards its long-term average growth rate of 2% or so once the economy picked up. When this didn’t happen in 2012, they said it would happen in 2013; then in 2014; then in 2015.... As the OBR data shows, this faster rate of productivity growth was always just around the corner.

This phenomena been talked about for a few years as the productivity puzzle. Explanations are legion and there’s unlikely to be a single cause, and explanations based on what happened during the financial crisis are now looking increasingly unlikely. The OBR seemed at first to admit they have no easy explanation – productivity has slowed down throughout the G7, so the problem (and its causes) goes beyond the UK. But the OBR does hint at an explanation for the anaemic productivity growth of late. Business investment in the capital, necessary to improve worker productivity, was expected to grow in 2015 and 2016 but investment was much weaker than expected. The OBR also concede that they consistently under-estimated the strength of the UK labour market; the UK grew by working more, not by improving the productivity of the hours worked.

The consequence of lower productivity growth over the next few years will be lower future tax receipts and so less financial leeway at a time when there may be bills to pay (although of course politically ambitious expenditure promises will require more tax rises to fund them). This apparently technical correction will narrow the choices available to politicians, possibly for years.

So can government action raise productivity? To an extent, yes, especially by well-targeted investments in infrastructure, research, skills and management (see the article on People Skills). But, two years ago, the then-Chancellor launched a government productivity plan. Admittedly we didn't think much of it, and it’s a little unfair to judge it by short-run results, but productivity is now lower than when it was published.

Topics A-Z

Browse our A–Z catalogue of information, guidance and resources covering all aspects of people practice.

Bullying

and harassment

Discover our practice guidance and recommendations to tackle bullying and harassment in the workplace.

About the author

Mark Beatson, Senior Labour Market Analyst

Mark's respected labour market analysis and commentary strengthens the CIPD’s ability to lead thinking and influence policy making across the whole spectrum of people management and workplace issues.

Prior to joining the CIPD, Mark was an economic consultant and for over 20 years worked as an economist in the Civil Service, latterly at Chief Economist/Director level, in a range of Government departments including the Department for Business Innovation and Skills (BIS), the Department for Innovation, Universities and Skills (DIUS), the Department of Trade and Industry (DTI) and HM Treasury.

Read our submission to the UK’s Chancellor, ahead of the March 2024 budget statement

Evaluating the pros and cons of working in shared office spaces, and how they impact on productivity

Peter Cheese, the CIPD's chief executive, looks at the challenges and opportunities faced by today’s business leaders and the strategic priorities needed to drive future success

We outline the key pieces of legislation set to come into force in the UK and explain their implications for employers and employees

We examine people’s desired hours and how this compares to the hours they actually work

Employers’ reactions to pension proposal highlight concerns over cost, while the CIPD calls for focus on raising pension awareness among staff, the need for higher contributions and better understanding of value for money