With inflation hitting levels not seen in the UK for more than 40 years, it’s not surprising that the CIPD's Autumn 2022 Labour Market Outlook (LMO) finds that most employers (73%) surveyed expect their workers’ financial situation to get worse over the next 12 months. Though there’s more pessimism on this issue among public sector (81%) and voluntary sector (82%) organisations than in the private sector (70%). Indeed, since the start of 2022, the LMO finds 16% of employers reporting that there has been an increase in staff opting out of the pension plan or reducing their contributions.

That said, there are variations within the private sector. For example, large firms (72%) are more likely to predict the financial situation of their staff will worsen than small and medium (SMEs) firms (67%). By industry, manufacturing firms (78%) and wholesale, retail, and real estate companies (76%) are more likely to say that the financial wellbeing of their workers will deteriorate.

Our research also finds that many employers (42%) are already worried about the financial wellbeing of their staff, especially those in the public (46%) and voluntary (56%) sectors. Private sector employers are currently less worried (39%), but it’s likely that this concern will only increase over the coming months as inflation keeps on growing and the economic downturn starts to bite. By contrast, few firms (6%) are unworried about their employees’ financial wellbeing.

Given the concern about workplace financial wellbeing, our survey reveals that most employers (51%) report that this risk is now being discussed more by senior management, especially in the public (57%) and voluntary sectors (66%).

By contrast, just under half of all companies (48%) say that it’s being discussed more. Firms in information and communication (58%), finance and insurance (57%), and wholesale, retail, and real estate (52%) are more likely to be bucking this trend and discussing this issue more. There is also a divide by company size, with SMEs (40%) being less likely to report that senior management are discussing this risk more than large firms (55%).

Overall, one in four (25%) firms report that there’s been no change in how often this threat is being discussed, while few (7%) either say that senior management is discussing it less, or it’s not being discussed at all (11%).

However, at a time when many employees are struggling with inflation, our research also finds that most businesses (66%) predict that the jump in energy process will have a negative impact on their own finances, especially those in hotels, catering and restaurants/arts, entertainment, and recreation (80%); manufacturing (78%); transport and storage (75); and wholesale, retail and real estate (75%) sectors.

Despite their own cost struggles, more companies are confident (32%) that they will be able to support their employees’ financial wellbeing over the next 12 months than those who are not confident (23%).

However, there are stark differences by industry, with firms in the information and communication (48%); and finance and insurance (46%) sectors expressing more confidence in their ability to help their workers, while businesses in hotels, catering and restaurants/arts, entertainment, and recreation sector (30%) expressing the least confidence.

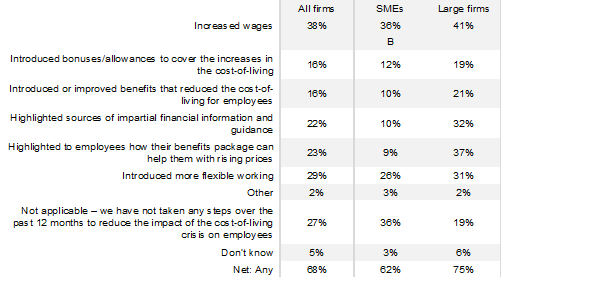

Increasing wages is the most common response to the cost-of-living crisis

Over the past 12 months, the most common responses in the private sector to aid workers during the cost-of-living crisis has been to increase wages (38%), introduce more flexible working (29%), highlighting to people how the employee benefits package can help them with rising prices (23%), and highlighting sources of impartial financial information and guidance (22%). In addition, some firms have given bonuses/allowances to cover the increase in the cost-of-living (16%) and some have introduced or improved benefits that cut the cost-of-living for employees (16%).

Within the private sector, firms in the manufacturing (45%); information and communication (42%); and wholesale, retail, and real estate (41%) sectors have been more likely to boost pay. Information and communication (45%) and business services, such as consultancy, accountancy, or law, (33%) have been more likely to introduce flexible working. Finance and insurance (36%) and wholesale, retail, and real estate (33%) firms have been most likely to highlight to their workers how the employee benefits package can help them with rising prices.

Overall, large companies have been more likely to have taken steps to reduce the impact of the cost-of-living crisis on their employees (75%) than SMEs (62%). While there is little difference in the proportion of large and SMEs taking such steps as increasing pay or introducing flexible working, there are significant differences in other areas, such as highlighting to employees how their benefits package can help them with rising prices, see Table 1.

Table 1: The steps taken by firms over the past 12 months to reduce the impact of the cost-of-living crisis on employees, by employer size

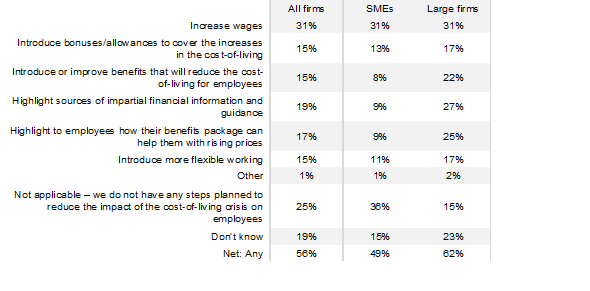

When it comes to next year, 31% of private sector employers plan to raise wages to help reduce the impact of the cost-of-living crisis, while 19% plan to highlight sources of impartial financial information and guidance, and 17% intend to highlight how their benefits package can help employees with rising prices.

Within the private sector, manufacturing companies (41%) and finance and insurance firms (40%) are most likely to be planning to increase wages in response to the cost of living. Information and communication firms (28%) are most likely to plan to highlight sources of impartial financial information and guidance to their staff, firms in this sector are also most likely to highlight how their benefits package can help employees with rising prices (31%), followed by utility companies (26%).

Large businesses are more likely to plan to take steps in the coming months to reduce the impact of the cost-of-living crisis on their workers (62%) than SMEs (49%).

While there is little difference in the proportion of large and SMEs taking such steps as increasing pay, again there are significant differences in other areas, such as flagging sources of impartial financial information and guidance and highlighting to employees how their benefits package can help them with rising prices, see Table 2.

Table 2: The steps firms plan to take over the next 12 months to reduce the impact of the cost-of-living crisis on employees, by employer size

Other company interventions adopted by employers to help promote financial wellbeing in the workplace include:

- asking staff at least once a year for their feedback on their pay and benefits (46%);

- actively measuring staff understanding about the pay and benefits on offer at least once a year (38%);

- encouraging employees to talk about their money concerns in the workplace (35%);

- targeting communications about employee benefits and financial education to specific groups of workers (33%);

- supporting and developing line managers so they can talk to staff about financial wellbeing (33%); and

- asking workers about their financial wellbeing at least once a year (30%).

While there is little difference between large firms and SMEs when it comes to encouraging staff to talk about their money worries in the workplace, there are some notable differences in other areas. For example, large companies are more likely: (55%) to ask employees for their feedback on the pay and benefits provided than SMEs (36%); (45%) to target communications about employee benefits and financial education to specific groups of workers than SMEs (21%); (46%) to measure the understanding of staff about the pay and benefits on offer than SMEs (30%); and (38%) to ask employees about their financial wellbeing than SMEs (22%).

How employers can make a difference

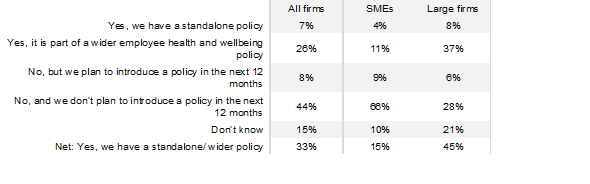

To support employee financial wellbeing and reduce the risk of in-work poverty, the CIPD is encouraging employers to focus on paying a fair and liveable wage; offering financial wellbeing benefits; and providing opportunities for in-work progression. Ideally, this should be brought together as a policy. Our Labour Market Outlook finds that 33% of private sector employers have already adopted either a standalone policy (7%) or have included it within a wider health and wellbeing policy (26%), while a further 8% have plans to create one in the coming months.

Having a policy can bring benefits. While the CIPD report Financial wellbeing: an evidence review finds that a policy can help boost employee wellbeing and their work performance, the CIPD’s 2022 Reward management survey also finds that staff take the existence of such a policy into account when thinking about their next job move, especially if they are already covered by a wellbeing policy.

Table 3: The proportion of private sector employers that have a financial wellbeing policy, by employer size

The data from the CIPD’s LMO also suggests that compared with large firms, many SMEs could be missing a trick by either not highlighting sources of impartial financial information to their workers and guidance, or by not highlighting to staff how their benefits package can help them with rising prices. Both are relatively low-cost ways of boosting employee financial wellbeing. Flexible working can also be another low-cost way for SMEs to promote financial wellbeing, so HR teams should review all forms of flexible working to see if it could be beneficial to both workers and the organisation.

You can also read about my thoughts on the cost-of-living crisis in my recent CIPD Voice On… blog.

Topics A-Z

Browse our A–Z catalogue of information, guidance and resources covering all aspects of people practice.

Bullying

and harassment

Discover our practice guidance and recommendations to tackle bullying and harassment in the workplace.

About the author

Charles Cotton, Senior Performance and Reward Adviser

Charles has recently led research into the business case for pensions, how front line managers make and communicate reward decisions, and managing reward risks, as well as the creation of a good practice guide on the annual pay review process. He is also responsible for the CIPD’s public policy work in the area of reward and is a Chartered Fellow of the CIPD.

Explore the CIPD’s point of view on low pay and financial wellbeing, including recommendations for employers and actions for the UK Government

Learn about the UK law surrounding workplace pensions and how to choose new schemes or review existing pension arrangements

Peter Cheese, the CIPD's chief executive, looks at the challenges and opportunities faced by today’s business leaders and the strategic priorities needed to drive future success

We outline the key pieces of legislation set to come into force in the UK and explain their implications for employers and employees

We examine people’s desired hours and how this compares to the hours they actually work

Employers’ reactions to pension proposal highlight concerns over cost, while the CIPD calls for focus on raising pension awareness among staff, the need for higher contributions and better understanding of value for money