This guide, produced in collaboration with law firm Lewis Silkin, focuses on self-employed contractors. Although the term ‘self-employed’ is not defined in legislation, it is generally accepted to apply to those individuals who run and manage their own business and who would, for example, have control over how, and when, they do the work and who carries it out. They would also negotiate a price for the work to be carried out.

Businesses and individuals should be aware that a self-employed individual may be categorised as self-employed for tax purposes but be considered an ‘employee’ (or more likely a ‘worker’) under employment law and therefore entitled to certain statutory rights and protections. Further, where an individual’s services are provided to a business client via a ‘personal services company’, certain tax-related obligations will be triggered under the IR35 regime.

This guide is designed to help employers understand the relationship that they have with their self-employed contractors and highlights any legal issues that they may come across. It also includes information and key points for self-employed individuals to help them understand their employment status and rights.

Self-employment and an overview of the law

Employment status - where do the self-employed fit in?

Summary of key rights and protections

Employing an individual versus engaging a self-employed contractor – the advantages and disadvantages

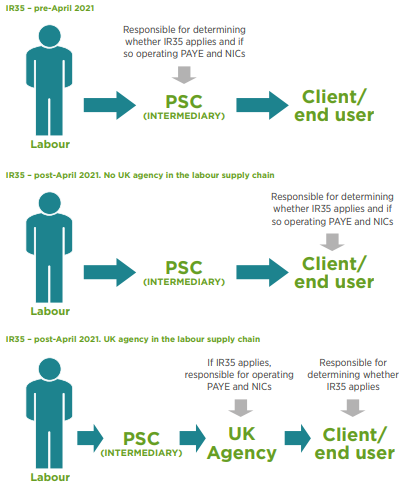

Tax and contractors

How to decide what contract to use

Acknowledgments

CIPD Trust

Tackling barriers to work today whilst creating inclusive workplaces of tomorrow.

Bullying

and harassment

Discover our practice guidance and recommendations to tackle bullying and harassment in the workplace.

What this practice is, why you should avoid it, and how to approach it if no other options are available

The 'Retained EU law bill', or REUL, changes UK employment law.

The CIPD's dedicated legal resource on holiday entitlement for all types of worker. This page includes guidance on applying the working time directive and how the UK court system sees legal claims against employers on annual leave matters.

What this practice is, why you should avoid it, and how to approach it if no other options are available

This guide has been developed for people professionals who want to maximise the benefits of flexible working within their organisations, incorporating flexibility into people plans, strategy, and their employee value proposition.

Practical guidance to help employers create a carer-friendly workplace

A guide for employees to develop a strong business case for submitting a flexible working request