The ONS’ latest labour market statistics are promising:

- At 75.8%, employment is at its highest rate since records began;

- The unemployment rate at 4% is the lowest it’s been since the 1970s; and

- The UK has the highest number of job vacancies on record at 870,000.

The CIPD’s latest Labour Market Outlook agrees with these impressive numbers, showing that employers expect to increase their workforce in the first quarter of 2019. And yet, despite these good news stories, few would describe the national mood as optimistic. Perhaps that is because interspersed between these golden headlines are stories like this:

- Productivity is 22.3% lower than it would be if the pre-financial crash trend had continued,

- Median annual earnings are still 3.2% lower than in 2008, and

- Honda has recently announced it will close its Swindon plant in 2021 with the loss of 3,500 jobs.

So, Is the UK labour market a good news story or not?

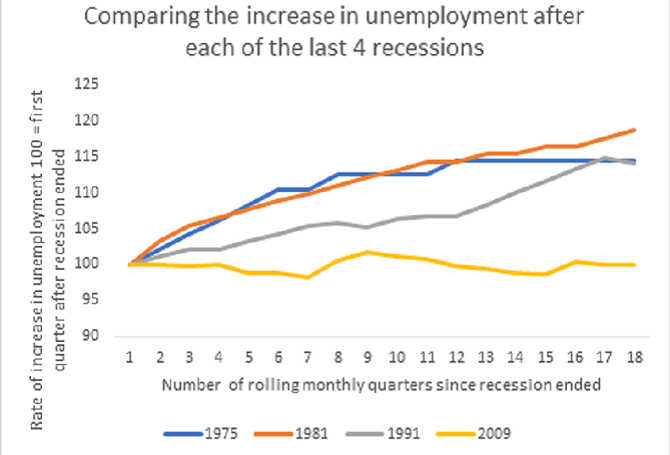

After the financial crash, policymakers were braced for a sharp increase in unemployment, but unlike in previous recessions, it remained muted.

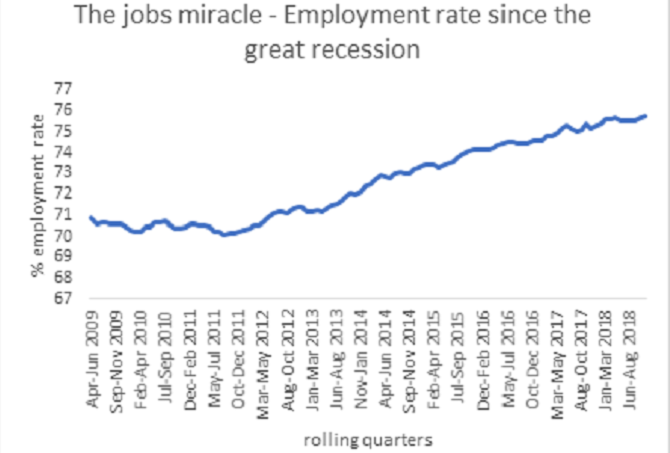

At the same time, employment steadily rose as part of a ‘jobs miracle’ that has continued to this day. High unemployment is not nice. There are economic and social consequences which for individuals can be long term, so the jobs miracle was unequivocally a win for the UK. Despite anxiety around insecure forms of working, much of the increase in employment has been made by full-time roles.

But every rose has its thorn. Before we talk about Brexit (and we will talk about Brexit) we should give some consideration to productivity. Like unemployment, low productivity is an economic bogeyman. However, whilst unemployment is ephemeral dissipating as the business cycle picks up, stagnant productivity has become entrenched.

Productivity is the engine that drives the economy forward. It is how businesses combine inputs in the production process and is therefore a measure of efficiency. More efficient businesses can afford to pay more and so productivity drives improvements in pay and living standards. It is no exaggeration to suggest that low productivity is the most pressing economic problem of our time.

Since the referendum

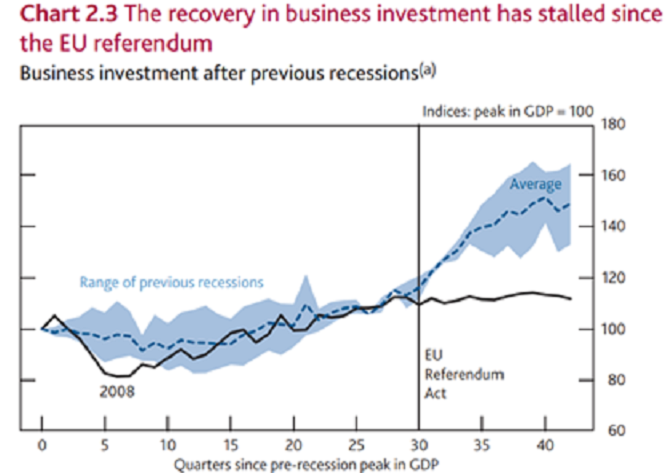

The Bank of England has suggested that since the EU referendum business investment has stalled, reflecting the uncertainty of Brexit. This is important because investment in things like plants and machinery can drive productivity growth. Gertjan Vlieghe, a member of the Bank of England’s Monetary Policy Committee that sets the Bank’s base rate, suggested in a speech in February that business may be substituting big investments for investing in people.

Buying specialised equipment is costly to reverse and so such decisions are put off in uncertain conditions whereas employment decisions are less costly to reverse. Businesses may be meeting demand by expanding their workforce instead of investing in technology to be more productive.

Sources: ONS and Bank calculations

(a) Chained volume measure. Recessions are defined as at least two consecutive quarters of negative GDP growth. Previous recessions include those beginning in 1973, 1975, 1980 and 1990. A recovery ends if a second recession occurs in the period shown.

The official figures from the ONS only take us up until the end of 2018, and the latest report from the CIPD covers the period up until the end of March: Brexit D-Day. Anecdotal and survey evidence suggests that recruitment started to deteriorate in January 2019. The recruitment planning horizon, especially for SMEs, is now past the Brexit deadline and some may be holding steady.

The implication for policymakers is obvious. Businesses are craving certainty and the lack of it is already starting to bite both in terms of investment and likely recruitment.

What can businesses do?

One of the biggest costs of Brexit has been the opportunity cost as businesses and government divert attention away from competing priorities. When the Brexit distraction goes away we will still be left with deep-seated structural impediments to growth such as struggling productivity, and it is here that employers may be able to make a real difference. We have talked about productivity as being how businesses combine inputs in the production process. In the impersonal language of economics, we might forget that those inputs include people even though labour is the largest cost for UK businesses.

It is therefore no wonder that a growing body of research, including a recent study by the ONS, has shed light on the important role of people management practices in boosting productivity. Getting the most out of your existing workforce is an attractive proposition, especially for firms reticent to hire in the face of uncertainty. Good people management is about having structured practices in place around such things as performance reviews, training and managing underperformance. The introduction of such practices can be particularly beneficial to SMEs.

Conclusion

The UK labour market has been a mixed bag, but the jobs miracle has been cause for celebration. To ensure it continues we should look long term, beyond Brexit, and work towards creating the conditions for long term prosperity. The people profession has a key role to play given the growing volume of research demonstrating the link between good people management and productivity.

Topics A-Z

Browse our A–Z catalogue of information, guidance and resources covering all aspects of people practice.

Bullying

and harassment

Discover our practice guidance and recommendations to tackle bullying and harassment in the workplace.

About the author

Jon Boys, Labour Market Economist

Jon joined the CIPD in January 2019 as an Economist. He is an experienced labour market analyst with expertise in pay and conditions, education and skills, and productivity.

Jon primarily uses quantitative techniques to uncover insights in labour market data, both publicly available and generated through in house surveying. Jon regularly contributes commentary and analysis of economic issues on the world of work to online, print and TV media. Recent work includes the creation of an international ranking of work quality, analysis of firm level gender pay gap reporting data, and an ongoing programme of work looking at the changing age profile of the UK workforce.

Peter Cheese, the CIPD's chief executive, looks at the challenges and opportunities faced by today’s business leaders and the strategic priorities needed to drive future success

Insight from the CIPD’s survey into factors driving pay decisions in UK workplaces and recommendations for practice

We examine people’s desired hours and how this compares to the hours they actually work

Peter Cheese, the CIPD's chief executive, looks at the challenges and opportunities faced by today’s business leaders and the strategic priorities needed to drive future success

We outline the key pieces of legislation set to come into force in the UK and explain their implications for employers and employees

We examine people’s desired hours and how this compares to the hours they actually work

Employers’ reactions to pension proposal highlight concerns over cost, while the CIPD calls for focus on raising pension awareness among staff, the need for higher contributions and better understanding of value for money